What Financial Controls Should Parent Groups Include in Bylaws?

Financial controls are rules that protect the group’s money and protect the volunteers handling it. Good bylaws require more than one person to approve or review financial activity, document reimbursements, and require regular reporting so members can see how funds are used.

What financial controls are

Financial controls are rules that govern how an organization collects, spends, and reviews money. Parent groups include these rules in their bylaws to ensure transparency, prevent misuse of funds, and protect the volunteers handling financial responsibilities.

Good financial controls require more than one person to review financial activity, document reimbursements, and provide regular financial reporting to members.

Start here

Financial controls exist for a simple reason: money attracts problems.

Throw “PTO fraud” or “school fundraiser embezzlement” into Google and you will be shocked by how often it happens.

Parent-teacher groups handle thousands of dollars through fun runs, sponsorships, auctions, and school events. When controls are weak, that money can be mishandled, intentionally or accidentally.

Most volunteers are honest people trying to help their school. Good bylaws assume that and still put guardrails in place.

Financial controls make it harder for one person to misuse funds and easier for the group to catch problems early if they happen.

Your bylaws should clearly define how money is handled, who reviews it, and how the group stays transparent with members.

The goal is not to eliminate every possible risk. The goal is to make financial activity visible, accountable, and difficult to abuse.

What financial controls mean in plain English

Financial controls are simple steps your parent group follows when handling money to ensure transparency and accountability.

For example:

- one person should not be able to move money without oversight

- reimbursements should require documentation (saying “I spent $1,000 on balloons, can the treasurer write me a check?” is not enough)

- members should regularly see financial reports

Financial rules that prevent most problems

-

Two authorized signers on bank accounts At least two officers should be authorized to sign checks or approve payments.

Example: the treasurer and president are both listed on the bank account after each election.

This prevents a single person from having full control over the account.

-

Separation of spending and review The person making payments should not be the only person reviewing the records.

Example: the treasurer issues payments, and the vice president or secretary reviews monthly statements.

This creates a second checkpoint and catches errors early.

-

Written reimbursement rule with receipts Reimbursements should require a standard process and proof of purchase.

Example: submit a reimbursement form and itemized receipt within 30 days.

This reduces disputes and keeps records consistent.

-

Unbudgeted spending cap Bylaws should define how much the board can approve without a full member vote.

Example: the board can approve up to $250 outside the budget; larger amounts require a member vote.

This prevents large surprise purchases.

-

Monthly treasurer report requirement The treasurer should provide regular reporting to the board and members.

Example: opening balance, income, expenses, and closing balance are presented at each regular meeting.

This keeps the group informed and makes unusual activity easier to spot.

-

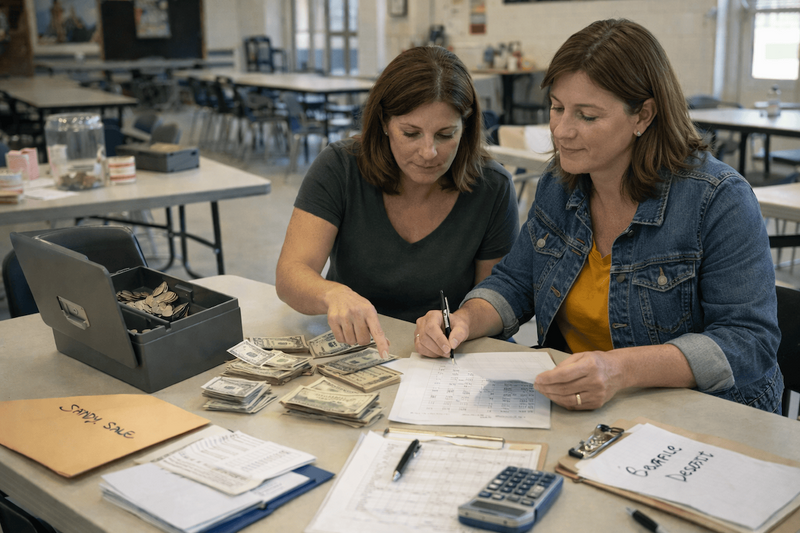

Dual control for cash handling Cash collected at events should always be counted and documented by more than one person.

Example: two unrelated volunteers count cash together and sign a count sheet.

This lowers the risk of mistakes or missing funds.

-

Annual financial review The group should schedule a yearly review of financial records by people who are not account signers.

Example: two non-signers review bank records in June and report findings to members.

This provides independent oversight and improves year-end handoffs.

How groups set spending limits

Most groups define a spending limit the board can approve without a full member vote. Larger purchases typically require approval from the membership.

The exact number depends on the size of the group and the annual budget.

- Small PTO (annual budget under $15,000): unbudgeted cap $100.

- Medium PTO (annual budget $15,000 to $60,000): unbudgeted cap $250.

- Large PTO (annual budget above $60,000): unbudgeted cap $500 with monthly disclosure log.

Are these controls necessary?

Yes.

Parent groups operate on trust from families, sponsors, and the school community. Basic financial controls protect that trust.

They also protect the volunteers handling the money. When clear rules exist, the treasurer is not left making judgment calls alone. Everyone understands the process, and financial decisions are documented and visible.

Common financial control mistakes

-

Only one signer for convenience

Result: one person can move money without oversight.

-

No written spending cap

Result: large purchases become disputes after the fact.

-

No routine reporting cadence

Result: problems may go unnoticed for months.